Building a $1M portfolio requires smart choices about where to put your money, and the biggest debate today centers on real estate vs crypto. This guide is for investors who want to understand how these two powerhouse asset classes can work together—or against each other—in your million dollar investment plan.

You’ll discover why real estate stability has created generational wealth for decades, while crypto volatility offers explosive growth potential that can fast-track your timeline. We’ll break down the real numbers behind real estate investment strategies, show you how to build a cryptocurrency portfolio that doesn’t keep you up at night, and reveal the hybrid investment approach that combines the best of both worlds.

Get ready to explore portfolio diversification strategies that balance steady cash flow from properties with the growth potential of digital assets, plus learn how to assess investment risk so you can sleep well while your money works harder.

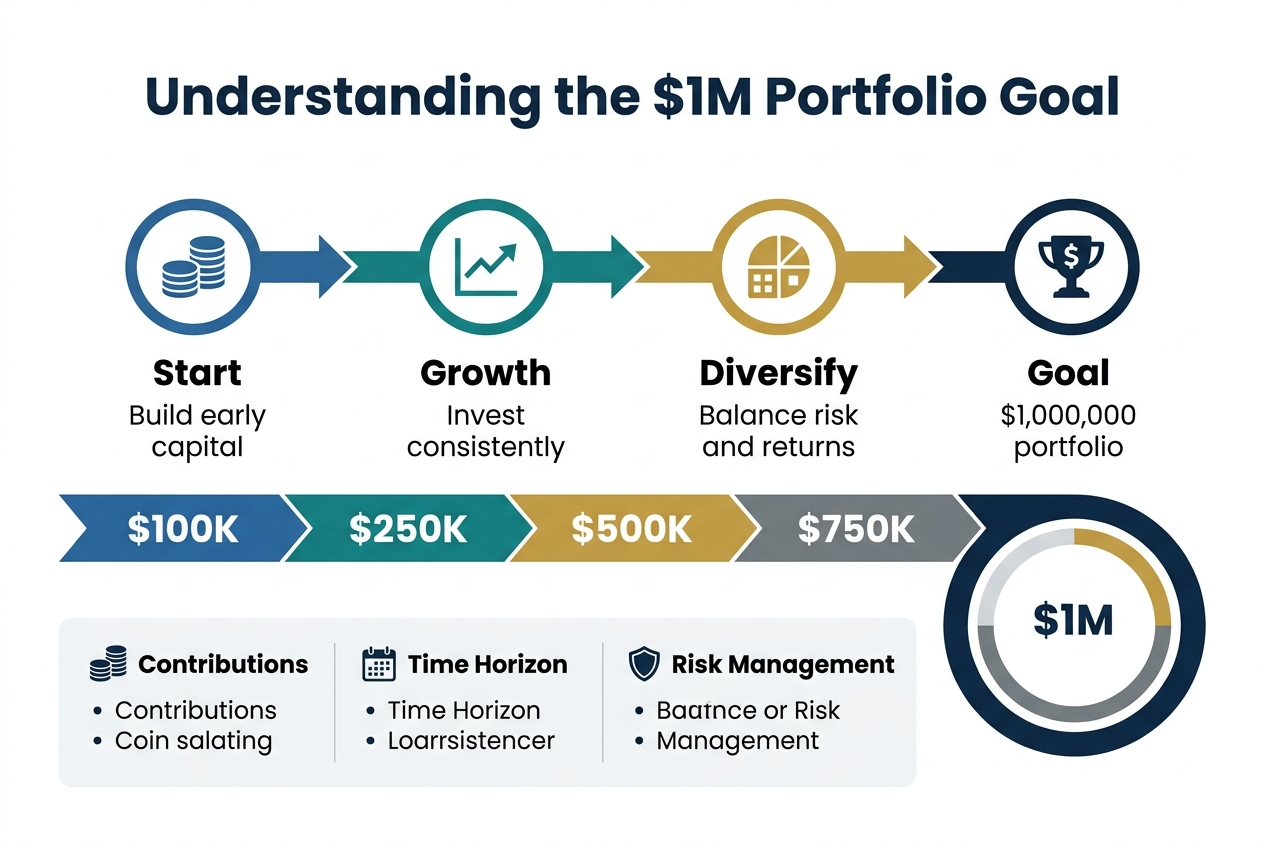

Understanding the $1M Portfolio Goal

Setting Realistic Timeframes for Wealth Accumulation

Building a $1M portfolio doesn’t happen overnight, despite what social media influencers might suggest. The timeline for reaching this milestone depends on several key factors: your starting capital, monthly contribution capacity, and chosen investment mix between real estate and crypto assets.

Most successful investors reach their million dollar portfolio within 10-20 years through consistent investing. If you’re starting with $10,000 and can invest $2,000 monthly with an average 8% annual return, you’ll hit the million-dollar mark in about 15 years. Bump that return to 12% through strategic real estate vs crypto allocation, and you could shave off 3-4 years.

The math works differently for various scenarios:

| Starting Amount | Monthly Investment | Average Return | Time to $1M |

|---|---|---|---|

| $5,000 | $1,500 | 8% | 18 years |

| $25,000 | $2,500 | 10% | 12 years |

| $50,000 | $3,000 | 12% | 9 years |

Remember, crypto can deliver explosive returns but also crushing losses. Real estate provides steadier growth but requires larger initial investments. Your timeframe should account for both the stability of real estate investment strategies and the potential acceleration from cryptocurrency exposure.

Breaking Down the $1M Target into Achievable Milestones

Smart wealth builders don’t fixate on the million-dollar finish line. They create stepping stones that make the journey manageable and motivating. Start by targeting these psychological milestones:

The First $100K (Years 1-5)

This stage feels the slowest because compound interest hasn’t kicked into high gear yet. Focus on maximizing your savings rate and establishing your hybrid investment approach. Many investors allocate 70% to real estate (REITs or rental properties) and 30% to crypto during this phase.

Quarter Million Mark ($250K)

At this point, your investments start working harder for you. Your cryptocurrency portfolio might represent 20-40% of total holdings, depending on market conditions and your risk appetite. Real estate continues providing stability through rental income or appreciation.

The Half Million Milestone ($500K)

This is where wealth building accelerates dramatically. Your portfolio generates significant passive income, allowing you to reinvest larger amounts. Many investors begin exploring direct real estate purchases or increasing their crypto positions during market downturns.

The Final Push ($500K to $1M)

The last stretch often takes less time than reaching the first $500K due to compound growth. Your portfolio diversification strategy becomes crucial here, balancing growth opportunities with wealth preservation.

Identifying Your Risk Tolerance and Investment Horizon

Your investment risk assessment determines whether you lean toward real estate stability or embrace crypto volatility. This decision shapes every aspect of your million dollar investment plan.

Conservative Investors (Low Risk Tolerance)

If market swings keep you awake at night, prioritize real estate-heavy allocations. Consider 80% real estate investments (REITs, rental properties) and 20% cryptocurrency. Your timeline might extend to 15-20 years, but you’ll sleep better during market turbulence.

Moderate Risk Investors

Most successful wealth builders fall into this category. A 60-40 split between real estate and crypto provides growth potential while maintaining stability. This balanced approach typically achieves the $1M goal within 10-15 years.

Aggressive Investors (High Risk Tolerance)

If you can stomach significant volatility for potentially faster wealth accumulation, consider 40% real estate and 60% crypto allocation. This strategy could reach $1M in 7-12 years but requires strong emotional discipline during market crashes.

Your investment horizon matters just as much as risk tolerance. Investors under 35 often favor higher crypto allocations since they have decades to recover from potential losses. Those closer to retirement typically emphasize real estate stability to preserve accumulated wealth.

Age-Based Allocation Guidelines:

- 20s-30s: 50-70% crypto, 30-50% real estate

- 40s: 60% real estate, 40% crypto

- 50s+: 70-80% real estate, 20-30% crypto

The key lies in honest self-assessment. Can you watch your portfolio drop 40% without panic selling? Do you understand both asset classes well enough to make informed decisions? Your answers determine the right balance for your wealth building strategies.

Real Estate Investment Fundamentals

Leveraging Mortgage Financing to Amplify Returns

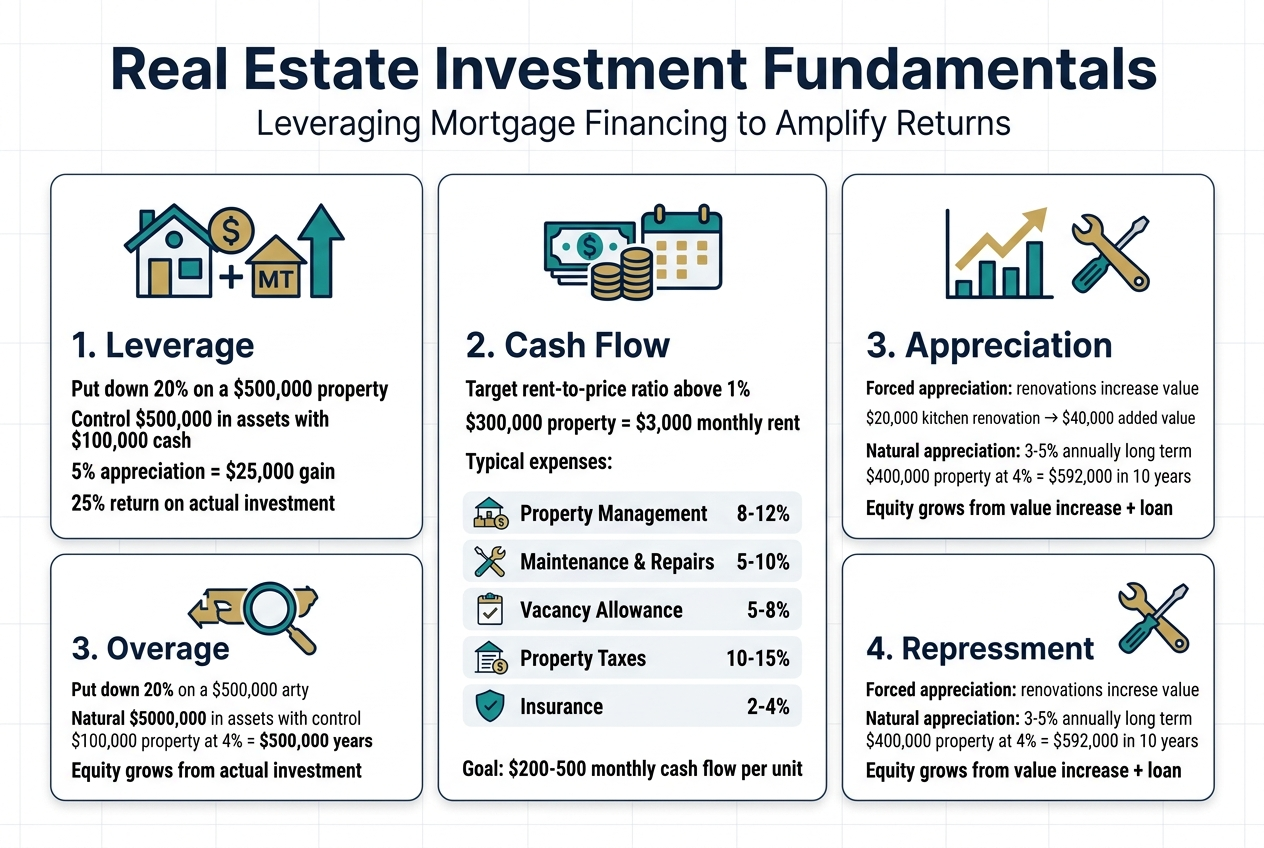

Real estate’s secret weapon for building wealth lies in its ability to work with borrowed money. When you put down 20% on a $500,000 property and finance the remaining $400,000, you’re controlling half a million dollars’ worth of assets with just $100,000 of your own cash. This leverage multiplies your returns dramatically.

Picture this scenario: your property appreciates 5% annually, generating $25,000 in value increase. Since you only invested $100,000 of your own money, that’s a 25% return on your actual investment—five times better than if you’d bought the property outright. Mortgage rates often sit below inflation rates, meaning you’re essentially borrowing money that becomes cheaper over time while your asset appreciates.

Smart investors focus on properties where rental income covers most or all of the mortgage payment. This strategy, called house hacking or the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat), allows you to scale your real estate investment strategies rapidly. Each property becomes a stepping stone to the next, compounding your path toward that $1M portfolio.

Generating Consistent Cash Flow Through Rental Properties

Cash flow represents the lifeblood of successful real estate investing. Unlike stocks that only pay when you sell or receive dividends, rental properties deliver monthly income that can cover your personal expenses while building long-term wealth.

Strong rental markets typically show rent-to-price ratios above 1%, meaning a $300,000 property should generate at least $3,000 monthly rent. However, the real magic happens when you account for all expenses:

| Expense Category | Percentage of Rent |

|---|---|

| Property Management | 8-12% |

| Maintenance & Repairs | 5-10% |

| Vacancy Allowance | 5-8% |

| Property Taxes | 10-15% |

| Insurance | 2-4% |

After accounting for these costs, positive cash flow properties become wealth-building machines. Many successful investors target properties generating $200-500 monthly cash flow per unit. With ten such properties, you’re looking at $2,000-5,000 monthly passive income—money that arrives whether you’re working, sleeping, or traveling.

Building Equity Through Property Appreciation

Property appreciation works on two levels: forced appreciation through improvements and natural market appreciation. Forced appreciation gives you immediate control over your returns. A $20,000 kitchen renovation might add $40,000 in property value, creating instant equity.

Historical data shows real estate appreciates roughly 3-5% annually over long periods, but local markets can vary dramatically. San Francisco and Austin have seen decades of 7-10% annual appreciation, while some Midwest markets barely keep pace with inflation.

The compound effect of appreciation becomes powerful over time. A $400,000 property appreciating at 4% annually reaches $592,000 after ten years. Combined with mortgage paydown, your equity position grows from both directions—rising property values and decreasing loan balances.

Tax Advantages and Deduction Strategies

Real estate offers unmatched tax benefits that can dramatically improve your after-tax returns. Depreciation alone allows you to deduct 1/27.5th of your property’s value annually, often creating paper losses that offset your rental income and sometimes other income sources.

Key deductions include:

- Mortgage interest on investment properties

- Property taxes and insurance premiums

- Maintenance and repair costs

- Professional services like property management

- Travel expenses for property visits

- Home office deductions if you manage properties from home

Advanced strategies like 1031 exchanges allow you to sell appreciated properties and reinvest proceeds into larger properties without paying capital gains taxes. This tax deferment strategy helps serious investors scale their portfolios faster toward that million dollar portfolio goal.

Market Research and Location Selection Criteria

Location drives everything in real estate. The right neighborhood can make a mediocre property profitable, while the wrong location can sink even beautiful homes. Successful investors focus on areas showing consistent job growth, population increases, and infrastructure improvements.

Research employment data for your target markets. Cities with diverse job markets weather economic downturns better than single-industry towns. Look for areas with major employers, universities, or government facilities providing stable employment bases.

Population trends reveal long-term demand patterns. Growing populations need housing, driving both rents and property values higher. Check census data and local planning documents for development projects that might affect your investment area.

Transportation infrastructure creates value. Properties near public transit, major highways, or planned infrastructure improvements often outperform isolated locations. Amazon’s HQ2 announcement demonstrates how single corporate decisions can transform entire metro areas overnight.

School districts matter even for rental properties. Good schools attract families willing to pay premium rents and create stable tenant bases. Properties in top-rated school districts typically experience lower vacancy rates and stronger appreciation.

Cryptocurrency Investment Strategies

Diversifying across established and emerging digital assets

Building a robust cryptocurrency portfolio requires a strategic mix of established players and promising newcomers. Bitcoin and Ethereum remain the cornerstones of any serious crypto allocation, representing roughly 60-70% of your digital asset holdings. These battle-tested assets have survived multiple market cycles and proven their resilience.

The remaining 30-40% should target carefully selected altcoins with strong fundamentals and real-world applications. Layer 2 solutions like Polygon, decentralized finance protocols such as Uniswap, and smart contract platforms like Solana offer growth potential while maintaining reasonable risk profiles. Avoid the temptation to chase meme coins or tokens with no clear utility.

Your diversification strategy should span different crypto categories:

| Asset Category | Allocation % | Examples | Risk Level |

|---|---|---|---|

| Store of Value | 30-40% | Bitcoin | Low |

| Smart Contract Platforms | 20-30% | Ethereum, Solana | Medium |

| DeFi Protocols | 10-15% | Uniswap, Aave | Medium-High |

| Infrastructure | 10-15% | Chainlink, Polygon | Medium |

| Emerging Technologies | 5-10% | Selected AI/Gaming tokens | High |

Dollar-cost averaging to minimize volatility impact

Dollar-cost averaging (DCA) transforms crypto volatility from your enemy into your friend. Instead of trying to time the perfect entry point, you invest a fixed amount regularly regardless of price movements. This approach naturally reduces your average cost basis during downturns while maintaining consistent exposure during uptrends.

Set up automated purchases on reputable exchanges like Coinbase Pro or Kraken. Weekly or bi-weekly intervals work best for most investors, as they smooth out short-term price swings while maintaining sufficient frequency to capture trends. A $500 monthly DCA split across your chosen assets creates discipline and removes emotional decision-making from the equation.

Track your DCA performance using spreadsheets or portfolio apps like CoinTracker. This data becomes invaluable when assessing whether to adjust your allocation or increase investment amounts during significant market downturns.

Understanding market cycles and timing opportunities

Crypto markets move in predictable four-year cycles largely driven by Bitcoin’s halving events. These cycles create opportunities for savvy investors who understand the psychological and technical patterns that emerge.

Bull markets typically last 12-18 months, characterized by euphoria, mainstream media coverage, and exponential price increases. Bear markets extend 2-3 years, featuring pessimism, capitulation, and prices declining 80-90% from peaks. Recognizing these phases helps you adjust your strategy accordingly.

During bear markets, increase your DCA frequency and focus on accumulating quality assets at discounted prices. Bull markets call for taking profits incrementally and reducing position sizes as euphoria peaks. Watch key indicators like the Fear and Greed Index, on-chain metrics such as active addresses, and traditional technical analysis patterns.

Staking and yield farming for passive income

Cryptocurrency offers unique passive income opportunities through staking and yield farming that traditional investments can’t match. Staking involves holding proof-of-stake cryptocurrencies to validate network transactions, earning rewards typically ranging from 4-12% annually.

Ethereum 2.0 staking provides around 5% APY with minimal technical knowledge required through services like Lido or Rocket Pool. Solana, Cardano, and Polkadot offer similar opportunities with varying reward rates and lock-up periods. Always research the specific requirements and risks before committing funds.

Yield farming generates higher returns but carries increased complexity and risk. Platforms like Aave, Compound, and Yearn Finance allow you to lend cryptocurrencies or provide liquidity to trading pairs. Returns can reach 8-20% annually, but impermanent loss and smart contract risks require careful consideration.

Start conservatively with established staking protocols before exploring more advanced yield farming strategies. Never stake more than 50% of your crypto holdings, maintaining liquidity for market opportunities and unexpected expenses. Track all staking rewards for tax purposes and consider the impact of lock-up periods on your overall portfolio flexibility.

Risk Assessment and Portfolio Protection

Real estate market stability and predictable returns

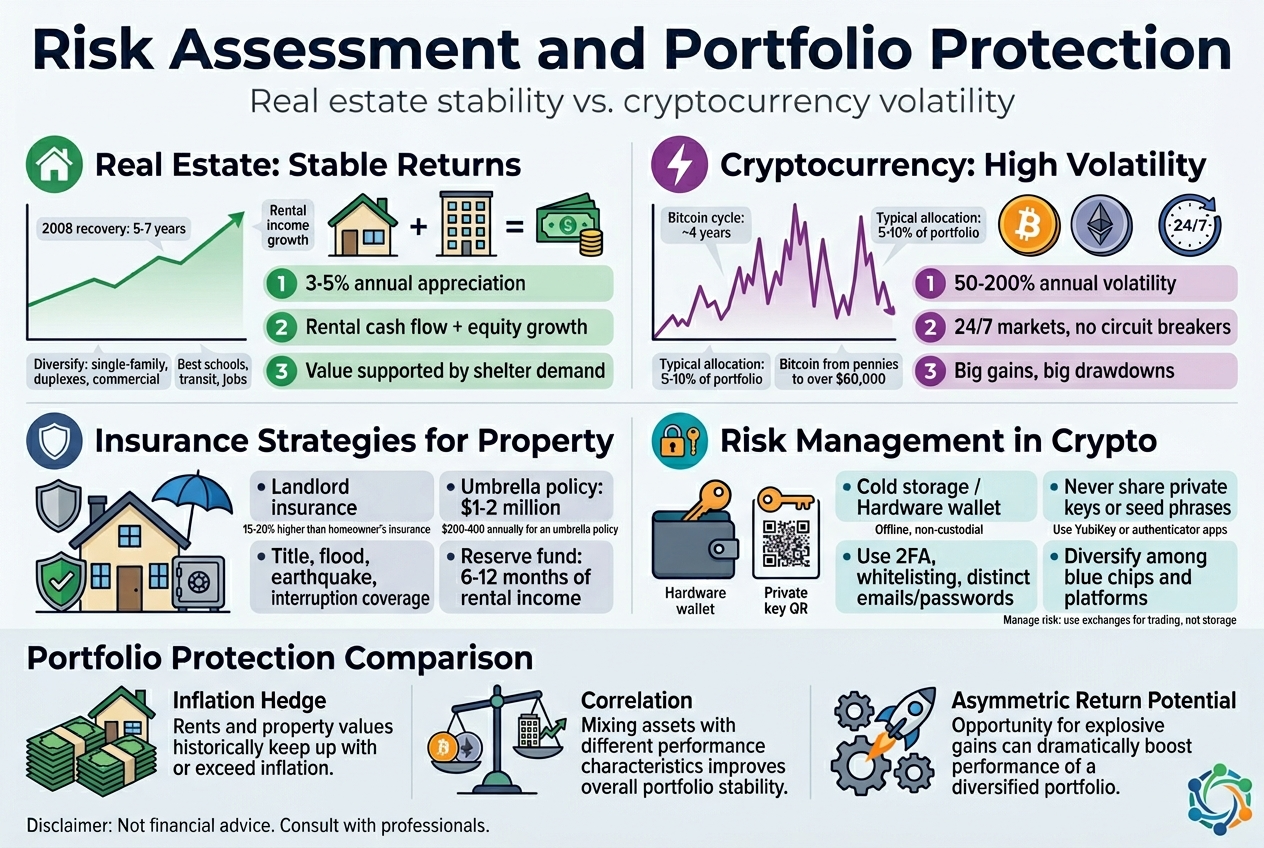

Real estate stands as one of the most stable investment vehicles for building a million dollar portfolio, offering predictable returns that have weathered numerous economic storms. Historical data shows that residential real estate typically appreciates at 3-5% annually over long periods, providing a solid foundation for wealth accumulation.

Property investments generate income through two primary channels: rental cash flow and property appreciation. Rental properties create monthly passive income that often covers mortgage payments while building equity. This dual benefit makes real estate particularly attractive for investors seeking consistent returns while working toward their $1M portfolio goal.

Market stability stems from real estate’s inherent value as a physical asset. People always need shelter, creating consistent demand regardless of economic conditions. Even during downturns, property values rarely drop to zero, unlike some investment vehicles. The 2008 housing crisis, while severe, saw most markets recover within 5-7 years, demonstrating real estate’s resilience.

Location plays a crucial role in stability. Properties in established neighborhoods with good schools, transportation, and employment opportunities maintain value better than speculative markets. Diversifying across different property types—single-family homes, duplexes, commercial properties—can enhance stability while spreading risk.

Cryptocurrency volatility and potential for massive gains

Cryptocurrency represents the opposite end of the investment spectrum, offering explosive growth potential alongside extreme volatility. Bitcoin’s journey from pennies to over $60,000 demonstrates the massive wealth-building potential that can accelerate your path to a million dollar portfolio, though the ride involves significant ups and downs.

Crypto markets operate 24/7 with no circuit breakers, meaning prices can swing 20-50% in single days. This volatility creates opportunities for substantial gains but also poses risks that can wipe out portfolios quickly. Smart crypto investors understand that timing and risk management are everything.

The key to cryptocurrency investment success lies in understanding market cycles and maintaining discipline during both euphoric highs and crushing lows. Bitcoin typically follows four-year cycles tied to halving events, while altcoins often experience even more dramatic swings based on technology adoption and market sentiment.

| Asset Class | Typical Annual Volatility | Potential Annual Returns | Time to Potential 10x |

|---|---|---|---|

| Real Estate | 5-15% | 6-12% | 20-30 years |

| Cryptocurrency | 50-200% | -80% to +1000% | 1-5 years |

Diversification within crypto helps manage volatility. Holding a mix of established coins like Bitcoin and Ethereum alongside promising altcoins can balance stability with growth potential. Many successful crypto investors allocate only 5-10% of their total portfolio to digital assets, treating them as high-risk, high-reward speculation.

Insurance strategies for property investments

Protecting real estate investments through comprehensive insurance strategies is non-negotiable when building a million dollar portfolio. Property insurance goes beyond basic homeowner’s coverage, requiring specialized protection that covers rental income loss, liability exposure, and property damage.

Landlord insurance provides essential coverage that standard homeowner’s policies exclude. This includes protection against tenant-caused damage, lost rental income during repairs, and liability claims from tenant injuries. The cost typically runs 15-20% higher than homeowner’s insurance but protects your investment income stream.

Umbrella policies offer additional liability protection beyond standard coverage limits. With rental properties, your exposure to lawsuits increases significantly. A $1-2 million umbrella policy costs roughly $200-400 annually but protects your entire portfolio from catastrophic claims.

Consider these additional protection strategies:

- Title insurance protects against ownership disputes and liens

- Flood insurance covers water damage in flood-prone areas

- Earthquake insurance provides protection in seismic zones

- Business interruption insurance covers lost rental income during major repairs

Self-insurance through reserve funds complements traditional insurance. Maintaining 6-12 months of rental income in reserve accounts covers deductibles, vacancy periods, and major repairs without disrupting cash flow.

Security measures for digital asset storage

Cryptocurrency security requires a completely different approach than traditional investments. Digital assets exist only as cryptographic keys, making proper storage the difference between building wealth and losing everything to hackers or human error.

Hardware wallets provide the gold standard for crypto security. These physical devices store private keys offline, making them immune to online attacks. Popular options like Ledger and Trezor cost $50-200 but protect investments worth thousands or millions. Think of hardware wallets as digital safety deposit boxes for your crypto holdings.

Never store significant crypto amounts on exchanges. While convenient for trading, exchanges remain prime targets for hackers. The collapse of FTX and numerous exchange hacks demonstrate why “not your keys, not your coins” is cryptocurrency’s golden rule. Use exchanges only for active trading, then immediately transfer holdings to secure storage.

Multi-signature wallets add another security layer by requiring multiple private keys to authorize transactions. This setup prevents single points of failure—even if one key is compromised, your funds remain secure. Many institutional investors require multi-sig protection for large crypto holdings.

Backup strategies are crucial since losing private keys means permanent loss of funds. Store seed phrases (backup words) in multiple secure locations—bank safety deposit boxes, fireproof safes, or even metal backup plates that survive fires and floods. Never store backups digitally or in cloud storage where hackers might access them.

Regular security audits help identify vulnerabilities before they become problems. Update wallet firmware, review backup procedures, and test recovery processes annually. The paranoia around crypto security isn’t excessive—it’s necessary for protecting your wealth building efforts.

Building Your Hybrid Investment Approach

Determining Optimal Allocation Percentages Between Assets

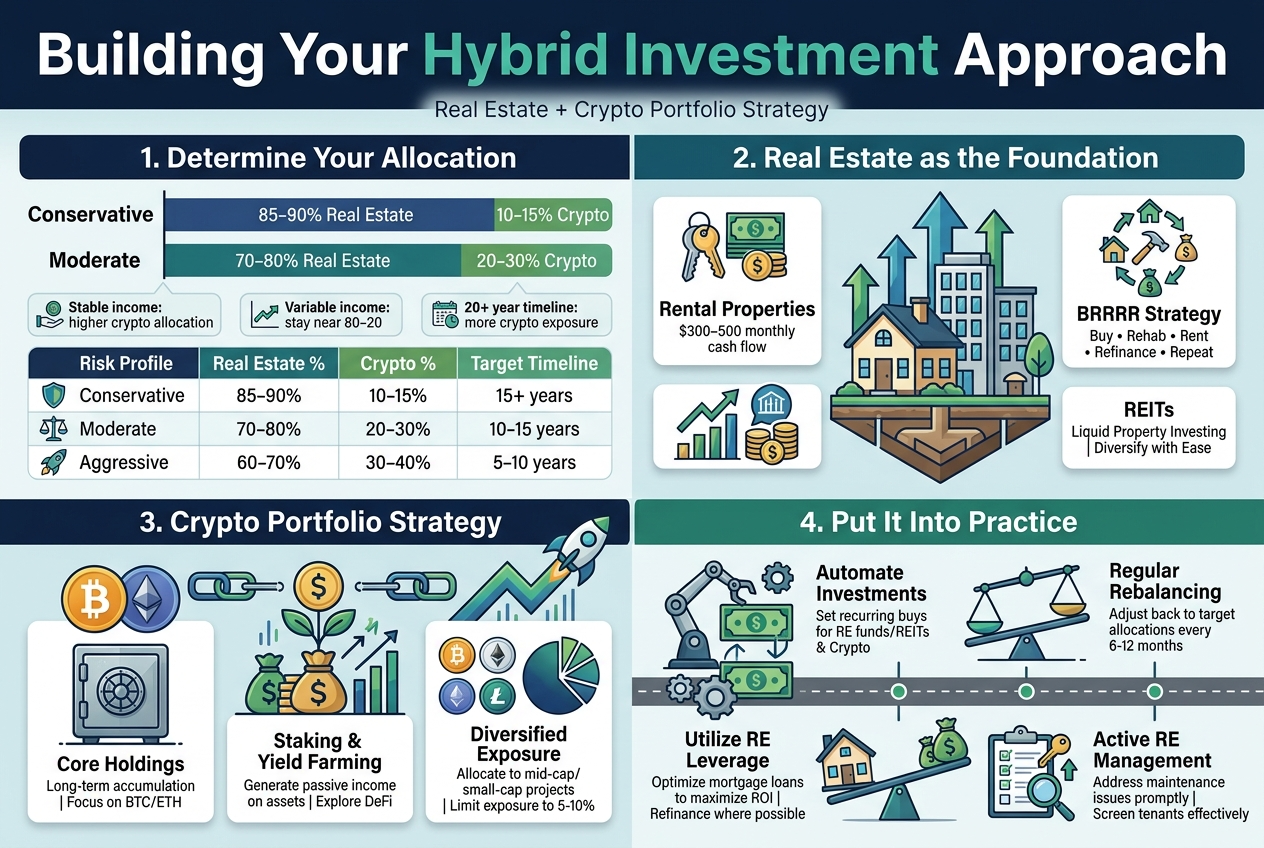

The sweet spot for most million dollar portfolio builders sits around a 70-30 or 80-20 split favoring real estate, though your specific allocation depends on your risk tolerance, age, and wealth-building timeline. Conservative investors approaching retirement might lean toward 85% real estate with just 15% in crypto, while aggressive younger investors could handle a 60-40 split or even 50-50 during crypto bull markets.

Your income level plays a huge role here. If you’re earning $150,000+ annually with stable employment, you can afford higher crypto allocations since you have consistent income to weather volatility. Those with variable income or lower earnings should stick closer to the 80-20 rule to protect their downside.

Consider your investment timeline when setting percentages. Building wealth over 20+ years allows for more crypto exposure since you can ride out multiple market cycles. Shorter timelines demand more conservative real estate-heavy allocations to protect against crypto’s notorious boom-bust cycles.

| Risk Profile | Real Estate % | Crypto % | Target Timeline |

|---|---|---|---|

| Conservative | 85-90% | 10-15% | 15+ years |

| Moderate | 70-80% | 20-30% | 10-15 years |

| Aggressive | 60-70% | 30-40% | 5-10 years |

Using Real Estate as Portfolio Foundation for Stability

Real estate serves as your portfolio’s bedrock because it generates predictable cash flow while appreciating steadily over time. Think of rental properties as your financial foundation – they keep money flowing into your portfolio even when crypto markets crash or stay flat for months.

Start with one solid rental property that cash flows $300-500 monthly after expenses. This creates a reliable income stream that compounds through reinvestment. Many successful investors use the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat) to rapidly scale their real estate holdings using the same initial capital multiple times.

REITs offer another stable foundation option for those who prefer hands-off investing. Dividend-paying REITs like Realty Income or Digital Realty Trust provide monthly or quarterly distributions while requiring zero property management effort. You can start with just $1,000 in REIT investments and gradually build your position.

Real estate investment strategies work best when you focus on cash flow first, appreciation second. Properties in growing suburban markets often provide the best balance of stability and growth potential. Look for areas with population growth, job creation, and limited housing supply to maximize your long-term returns.

Leveraging Crypto for Accelerated Growth Potential

Cryptocurrency serves as your portfolio’s growth engine, potentially turning years of wealth building into months during bull markets. Bitcoin and Ethereum remain the safest crypto investments for million dollar portfolio construction, with Bitcoin acting like digital gold and Ethereum powering the decentralized finance ecosystem.

Dollar-cost averaging works exceptionally well for crypto investments. Investing $500-1,000 monthly into Bitcoin and Ethereum regardless of price smooths out volatility while building substantial positions over time. This strategy prevents you from trying to time markets and removes emotional decision-making from your investment process.

Alternative cryptocurrencies can accelerate growth but require careful selection. Focus on projects with real-world utility, strong development teams, and growing adoption. Solana, Chainlink, and Polygon have demonstrated staying power beyond pure speculation, making them reasonable additions to a diversified crypto portfolio.

Staking provides additional income from your crypto holdings, similar to rental income from real estate. Ethereum, Cardano, and Solana all offer staking rewards ranging from 4-10% annually, adding another layer of returns to your portfolio while holding for long-term appreciation.

Rebalancing Strategies as Markets Evolve

Market cycles demand active portfolio management to maintain your target allocations and maximize wealth building opportunities. Crypto’s explosive bull runs often push portfolios heavily toward digital assets, creating dangerous concentration risk that smart investors address through systematic rebalancing.

Rebalance quarterly or when any asset class deviates more than 10% from your target allocation. If crypto runs from 20% to 35% of your portfolio, sell some crypto profits and buy more real estate to restore balance. This disciplined approach forces you to sell high and buy low automatically.

Time-based rebalancing works better than threshold-based for most investors since it removes emotion from decisions. Set calendar reminders for the first day of each quarter to review and adjust your allocations regardless of recent market performance.

Tax-loss harvesting during rebalancing can significantly boost your after-tax returns. Sell losing crypto positions to offset gains from profitable real estate sales or crypto trades. This strategy works especially well in tax-advantaged accounts where you can rebalance without immediate tax consequences.

Bear markets present the best rebalancing opportunities for aggressive wealth building. When crypto crashes 50-80% from peaks, gradually increase your crypto allocation above target levels to capitalize on oversold conditions. Smart money moves into quality assets when others are selling in panic.

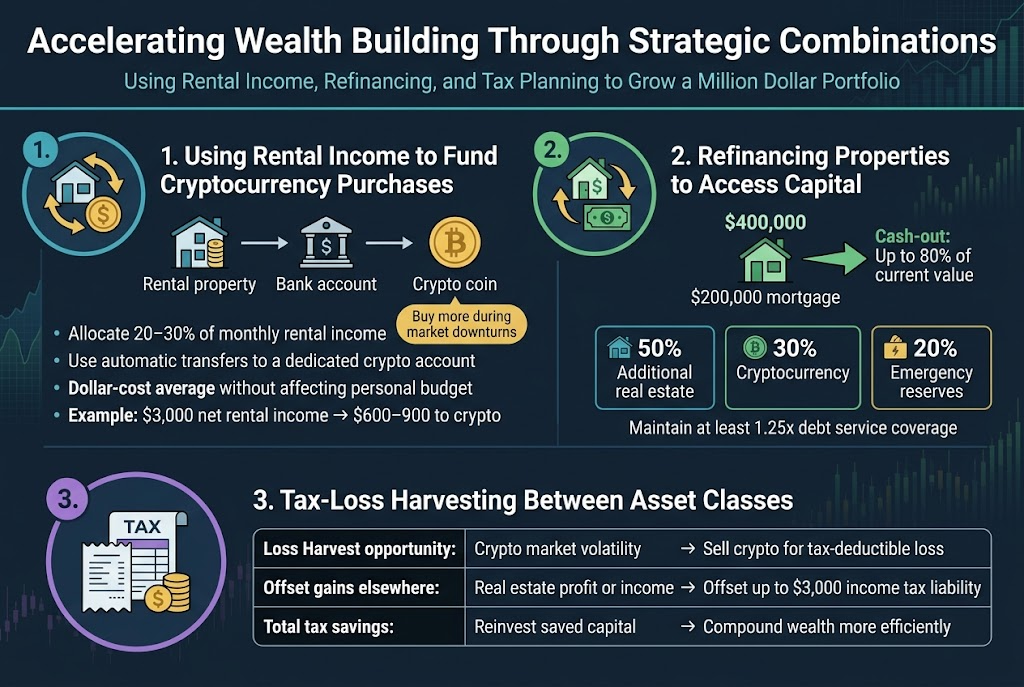

Accelerating Wealth Building Through Strategic Combinations

Using Rental Income to Fund Cryptocurrency Purchases

Smart investors have discovered a powerful wealth-building technique: channeling rental income directly into cryptocurrency investments. This approach creates a systematic funding mechanism that doesn’t require additional out-of-pocket cash while building your million dollar portfolio through strategic diversification.

The beauty of this strategy lies in its automatic nature. Once your rental properties generate consistent positive cash flow, you can establish a predetermined percentage to allocate toward crypto purchases. Many successful investors dedicate 20-30% of their monthly rental income to cryptocurrency, allowing them to dollar-cost average into digital assets without affecting their personal budget.

Consider setting up automatic transfers from your rental income account to a dedicated crypto investment account. This removes emotional decision-making and creates discipline in your investment approach. For example, if your properties generate $3,000 monthly in net rental income, allocating $600-900 toward cryptocurrency creates substantial accumulation over time.

The timing advantage becomes significant during market downturns. While crypto experiences volatility, your rental income remains relatively stable, allowing you to purchase digital assets at discounted prices when others are selling. This contrarian approach has proven highly effective for building substantial crypto positions within a diversified portfolio.

Refinancing Properties to Access Capital for Investments

Real estate refinancing presents one of the most powerful tools for accessing capital to expand your investment portfolio. When property values increase, refinancing allows you to extract equity while maintaining ownership of appreciating assets.

The current market offers unique opportunities for strategic refinancing. Properties purchased years ago have likely appreciated significantly, creating substantial equity. By refinancing at today’s rates, you can access this equity to invest in both additional real estate and cryptocurrency positions.

Cash-out refinancing typically allows you to access up to 80% of your property’s current value. If you own a property worth $400,000 with a $200,000 mortgage, you could potentially access $120,000 in cash ($400,000 × 0.80 = $320,000 minus the existing $200,000 loan).

This capital can be strategically deployed across multiple investment vehicles:

- 50% toward additional real estate: Down payments on new rental properties

- 30% toward cryptocurrency: Building substantial positions in established digital assets

- 20% emergency reserves: Maintaining liquidity for opportunities and protection

The key lies in ensuring your refinanced payment remains manageable with current rental income. Calculate debt service coverage ratios carefully, maintaining at least 1.25x coverage to ensure sustainable cash flow.

Tax-Loss Harvesting Between Asset Classes

Tax-loss harvesting between real estate and cryptocurrency creates powerful opportunities to optimize your tax burden while rebalancing your million dollar portfolio. This strategy involves strategically realizing losses in one asset class to offset gains in another.

Cryptocurrency’s volatility makes it particularly useful for tax-loss harvesting. Digital assets can be sold at a loss and immediately repurchased (no wash sale rules apply to crypto), allowing you to maintain your position while realizing tax benefits. These losses can offset real estate gains, including depreciation recapture when selling rental properties.

Real estate provides different tax optimization opportunities. Property sales can be timed to coincide with crypto gains, creating offsetting tax events. Additionally, 1031 exchanges allow real estate investors to defer taxes while moving between properties, freeing up capital for other investments.

| Strategy | Real Estate Application | Crypto Application | Tax Benefit |

|---|---|---|---|

| Loss Harvesting | Limited timing flexibility | Immediate execution | Offset capital gains |

| Gain Management | 1031 exchanges available | No deferral options | Defer taxes on RE gains |

| Depreciation | Annual tax deductions | No depreciation | Reduce taxable income |

Professional tax planning becomes essential when managing both asset classes. Work with advisors who understand digital asset taxation and real estate strategies. Proper documentation and timing can save thousands in taxes while optimizing your wealth building approach.

The hybrid investment approach combining real estate stability with crypto potential, enhanced by strategic tax planning, creates multiple pathways to accelerate your journey toward a million dollar portfolio.

Building a million-dollar portfolio doesn’t have to be an either-or choice between real estate and cryptocurrency. The smartest approach combines the steady, reliable growth of property investments with the explosive potential of digital assets. Real estate gives you that solid foundation – steady cash flow, tangible assets, and protection against inflation. Crypto, on the other hand, offers the chance for rapid gains that can fast-track your wealth-building timeline when managed carefully.

Your path to seven figures starts with understanding your risk tolerance and building a strategy that balances stability with growth potential. Start with real estate to create your base, then gradually add cryptocurrency exposure as you become more comfortable with the volatility. Remember, the wealthy didn’t get there by playing it completely safe or by gambling everything on high-risk bets – they found the sweet spot between the two. Take action today by evaluating your current financial position and deciding which asset class makes sense for your first major investment move.